Aug 2026: THE THIRD IAS-SBM JOINT WORKSHOP Financial Econometrics in the Big Data Era. - picture.

Jun 2026: Prof. Yingying Li presented 'Site Percolation Network Models for Event-Driven Systems' at 18th Annual Society for Financial Econometrics Conference (SoFiE 2026) in Macau. - picture.

Jun 2026: Prof. Xinghua Zheng presented 'A Factor Hypergraph Model for Stock Co-jump Process' at 18th Annual Society for Financial Econometrics Conference (SoFiE 2026) in Macau. - picture.

Jun 2026: Rohan Sen presented 'Kernel-Based Nonparametric Tests For Shape Constraints' at 18th Annual Society for Financial Econometrics Conference (SoFiE 2026) in Macau. - picture.

Jun 2026: Prof. Yingying Li served as a lecturer and keynote speaker at QFFE 2026 - Quantitative Finance and Financial Econometrics in Marseille, France. - picture.

May 2026: Prof. Xinghua Zheng was appointed as Associate Editor of the Journal of the American Statistical Association.

May 2026: Zhuoxi Li was awarded an RGC Junior Research Fellowship.

May 2026: Junkun Yang received the HKPFS.

May 2026: Ruizhao Huang received the Red Bird Academic Excellence Award.

Mar 2026: Welcome new member Rohan Sen to the lab as a Postdoctoral Researcher.

Feb 2026: Prof. Yingying Li appointed as AE of Management Science.

Jan 2026: Leheng Chen presented 'Efficient Portfolio Estimation in Large Risky Asset Universes' at the CityU Workshop in Econometrics and Statistics (Hong Kong).

Jan 2026: Welcome new member Yimeng Ren to the lab as a Postdoctoral Researcher.

Jan 2026: Prof. Xinghua Zheng appointed as AE of the Journal of Econometrics and Econometric Theory.

Dec 2025: Prof. Yingying Li, Prof. Xinghua Zheng, and Prof. Carsten H. Chong organized the 2025 Annual Meeting of the Greater Bay Econometrics Study Group.

Dec 2025: Shiman Hu presented 'Predicted Factor Model for Jump Intensities' at the 2025 Annual Meeting of the Greater Bay Econometrics Study Group (Hong Kong).

Dec 2025: Ruizhao Huang presented 'MAXSER-C' at the 2025 Annual Meeting of the Greater Bay Econometrics Study Group (Hong Kong).

Dec 2025: Leheng Chen presented 'Efficient Portfolio Estimation in Large Risky Asset Universes' at the 2025 Annual Meeting of the Greater Bay Econometrics Study Group (Hong Kong).

Dec 2025: Qi Fan presented his research at the 2025 Annual Meeting of the Greater Bay Econometrics Study Group (Hong Kong).

Dec 2025: Yingwen Tan presented his research at the 2025 Annual Meeting of the Greater Bay Econometrics Study Group (Hong Kong).

Dec 2025: Zhuoxi Li presented his research at the 2025 Annual Meeting of the Greater Bay Econometrics Study Group (Hong Kong).

Dec 2025: Prof. Yingying Li was named a Fellow of the Journal of Econometrics.

Nov 2025: Prof. Yingying Li was recognized as Fung Term Professor at HKUST's Eighth Inauguration Ceremony of Named Professorships. - picture.

Sep 2025: Prof. Yingying Li awarded NSFC YSF Cat-A.

Sep 2025: Welcome new members Jiawei Wu, Yuheng Wu, and Hongbao Zhang to the lab as Research Assistants.

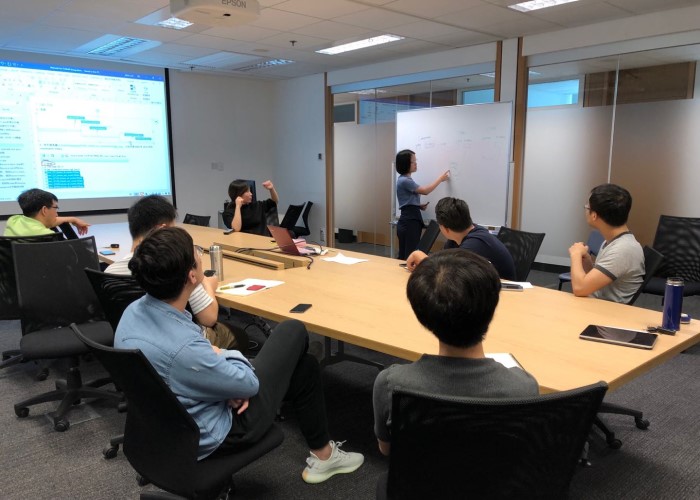

Aug 2025: Prof. Yingying Li, Prof. Xinghua Zheng, and Prof. Carsten H. Chong organized THE SECOND IAS-SBM JOINT WORKSHOP Financial Econometrics in the Big Data Era. - picture 1 2.

Aug 2025: Shiman Hu presented 'Predicted Factor Model for Jump Intensities' at the 2nd HKUST IAS-SBM Joint Workshop on Financial Econometrics in the Big Data Era (Hong Kong).

Aug 2025: Ruizhao Huang presented 'MAXSER-C' at the 2nd HKUST IAS-SBM Joint Workshop on Financial Econometrics in the Big Data Era (Hong Kong).

Aug 2025: Leheng Chen presented 'Efficient Portfolio Estimation in Large Risky Asset Universes' at the 2nd HKUST IAS-SBM Joint Workshop on Financial Econometrics in the Big Data Era (Hong Kong).

Aug 2025: Leheng Chen presented 'Efficient Portfolio Estimation in Large Risky Asset Universes' at the 2025 Random Matrix Theory and Applications Summer Workshop (Yunnan).

Aug 2025: Welcome new member Haoxuan Lu to the lab as a PhD student.

Aug 2025: Welcome new members Qi Fan, Yingwen Tan, and Zhuoxi Li to the lab as Postdoctoral Researchers.

Aug 2025: Leheng Chen successfully defended his PhD thesis and became Dr. Chen. - picture.

Jun 2025: Prof. Xinghua Zheng presented the paper 'Incorporating Return Prediction in High-dimensional Mean-Variance Portfolio Optimization' at the 17th Annual Society for Financial Econometrics Conference (SoFiE 2025) in Paris.

Jun 2025: Prof. Yingying Li presented the paper 'Predictive Factor Model for Jump Intensities' at the 17th Annual Society for Financial Econometrics Conference (SoFiE 2025) in Paris.

Jun 2025: Prof. Yingying Li served as a plenary speaker at the 19th International Symposium on Econometric Theory and Applications (SETA 2025) in Macau and gave the talk 'Learning the Stochastic Discount Factor'. - picture.

Jun 2025: Shiman Hu presented 'Predicted Factor Model for Jump Intensities' at the 19th International Symposium on Econometric Theory and Applications (SETA 2025) (Macau).

Jun 2025: Leheng Chen presented 'Efficient Portfolio Estimation in Large Risky Asset Universes' at the 19th International Symposium on Econometric Theory and Applications (SETA 2025) (Macau).

Jun 2025: Yibin Zhang successfully defended his PhD thesis and became Dr. Zhang.

May 2025: Haoxuan Lu received the HKPFS.

May 2025: Changlei Lyu successfully defended his PhD thesis and became Dr. Lyu. - picture.

Feb 2025: Prof. Yingying Li was named Fung Term Professor. - picture.

Jan 2025: Juncheng Li successfully defended his PhD thesis and became Dr. Li.

2025: Prof. Xinghua Zheng named Lee Hang Fellow.

Dec 2024: Bicheng Zhan and Junkun Yang joined FinStaR as Research Assistants in November and December.

Dec 2024: Leheng Chen presented 'Efficient Portfolio Estimation in Large Risky Asset Universes' at the First Macau International Conference on Business Intelligence and Analytics (Macau).

Nov 2024: Jian Yuan successfully defended his PhD thesis and became Dr. Yuan. - picture.

Jun 2024: Prof. Yingying Li and Prof. Torben Andersen co-chaired the 16th Annual Society for Financial Econometrics (SoFiE) Conference in Rio de Janeiro, Brazil. - picture.

Jun 2024: Leheng Chen presented 'Robust Large Portfolio Optimization with Heteroscedastic and Heavy-Tailed Returns' at the 16th Society for Financial Econometrics (SoFiE) Annual Conference (Rio de Janeiro).

May 2024: Prof. Yingying Li, Prof. Xinghua Zheng, and Prof. Carsten H. Chong organized a workshop on Financial Econometrics in the Big Data Era. - picture.

May 2024: Prof. Xinghua Zheng and Prof. Yingying Li spoke in the event "AI for Good" hosted by Chicago Booth. - picture 1 2 3 4.

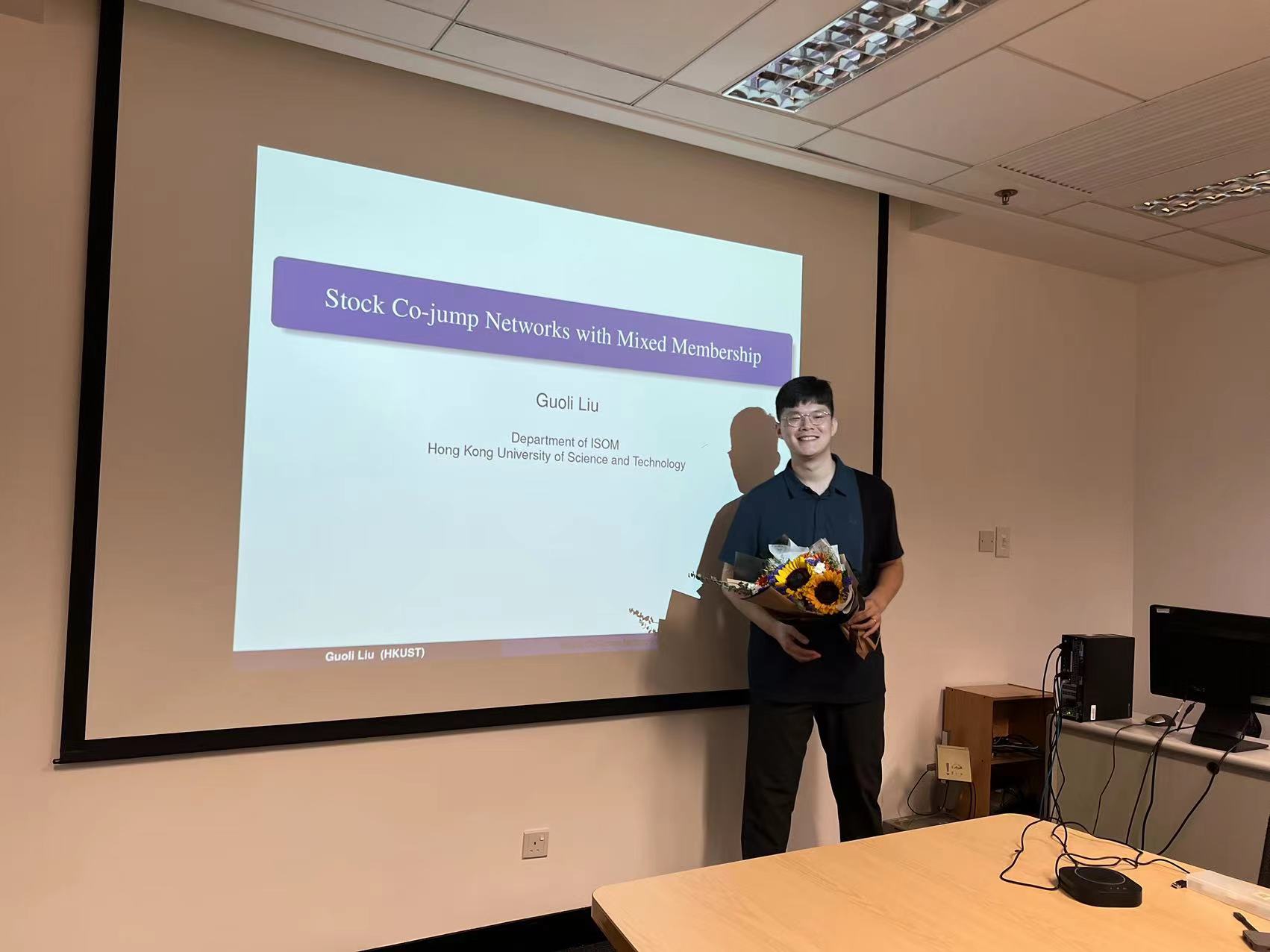

Aug 2023: Guoli Liu successfully defended his PhD thesis and became Dr. Liu. - picture 1 2.

Jul 2023: Prof. Yingying Li was promoted to Chair Professor.

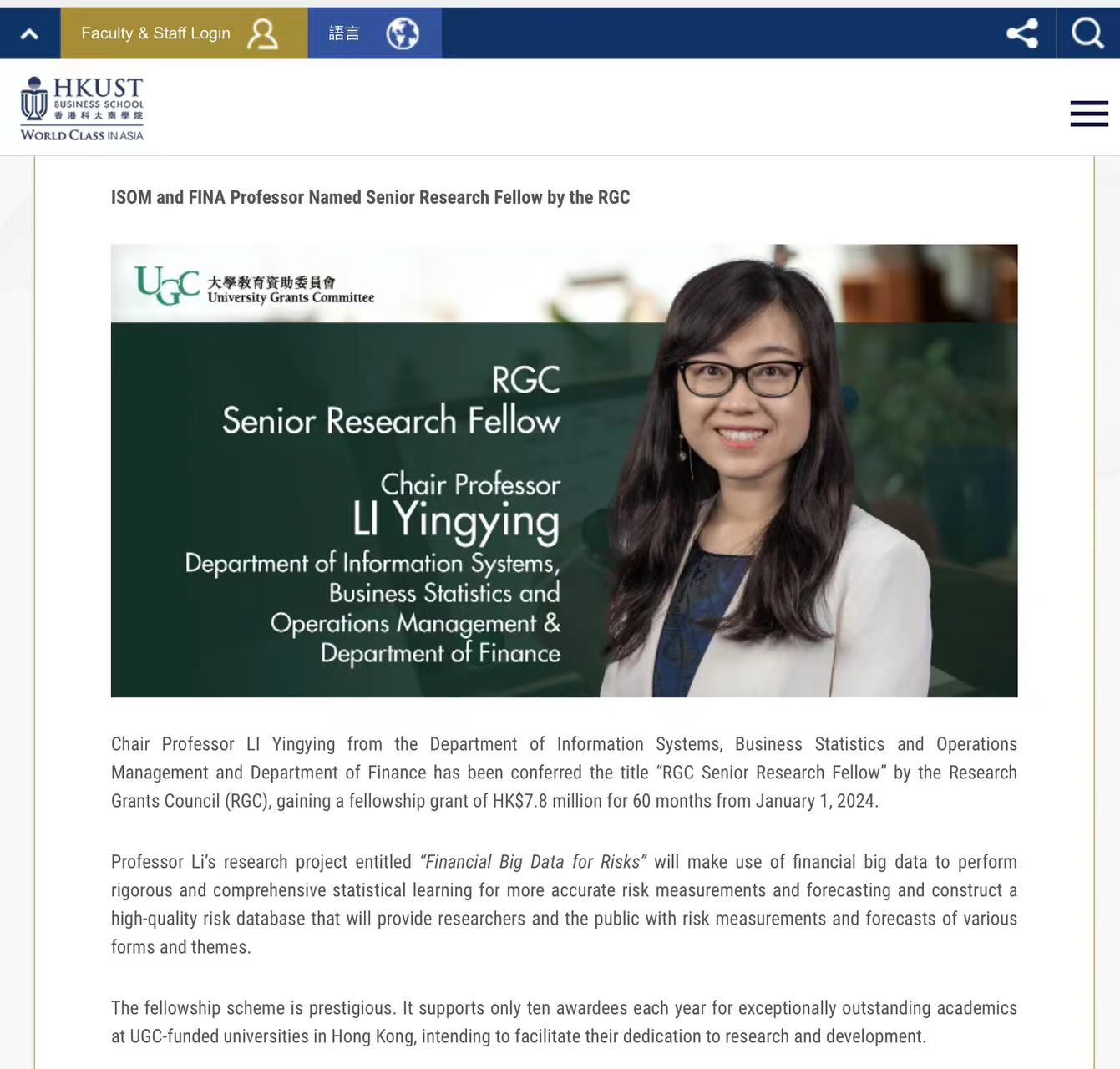

Jul 2023: Prof. Yingying Li was named Senior Research Fellow by the Research Grants Council. - picture.

Jun 2023: Prof. Xinghua Zheng elected as Fellow of the Society for Financial Econometrics (SoFiE). - picture.

Jun 2022: Guoli Liu won the Redbird Academic Excellence Award.

Jun 2022: Leheng Chen won the Redbird PhD Award.

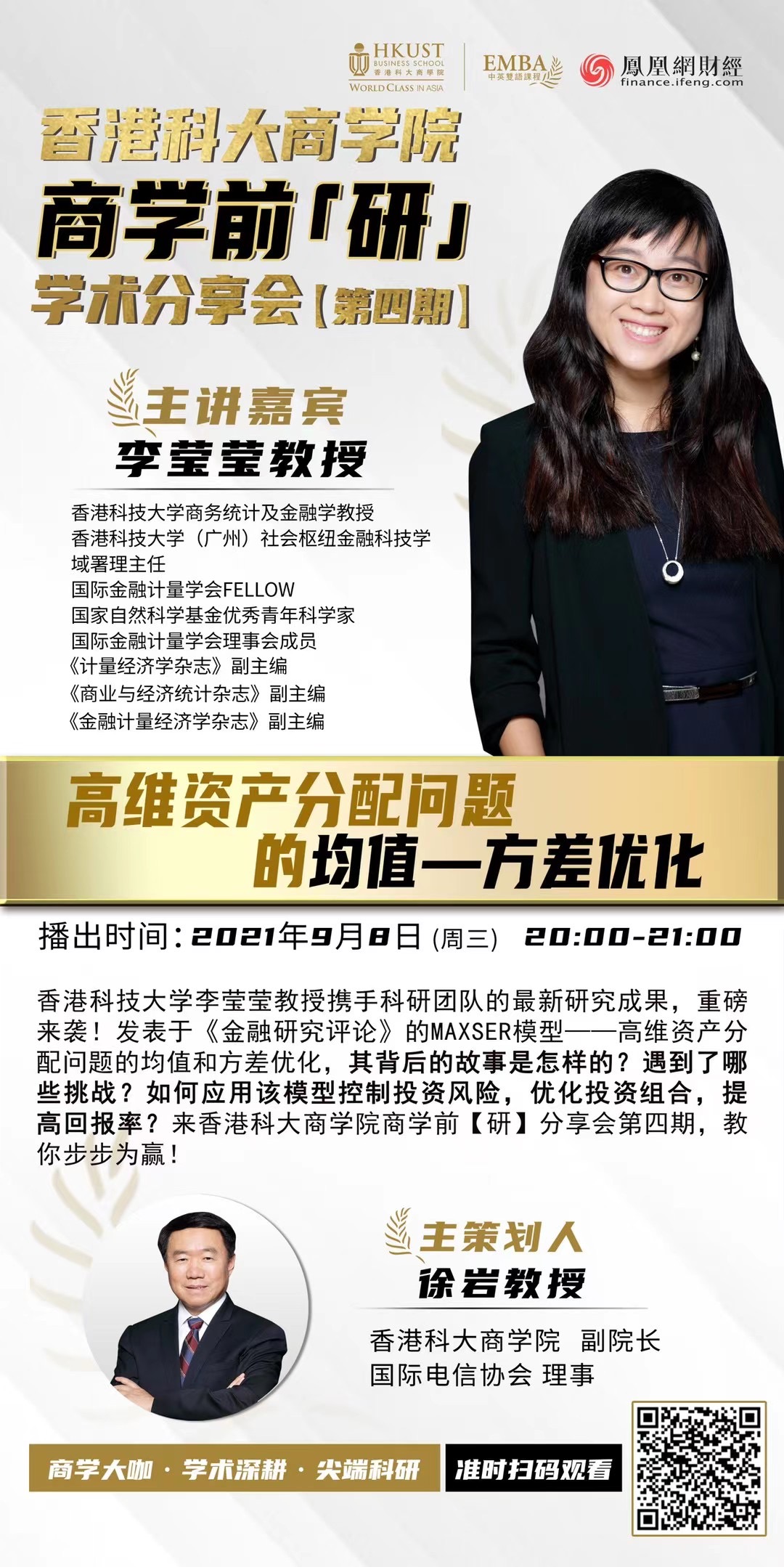

Sep 2021: Prof. Yingying Li gave a talk in the "Cutting-edge Research in Business Studies Series" Live Broadcast via

HKUST MBA China,

ifeng.com, sohu.com, Tencent (total 216,693 live stream views, watch replay). - picture.

Sep 2021: Welcome new member Ruizhao Huang to the lab.

Sep 2021: Welcome new PhD student Shiman Hu to the lab.

Jul 2021: Prof. Yingying Li was recognized as one of the faculty members who made exceptional achievements in the past academic year. - picture.

Apr 2021: Prof. Yingying Li gave a talk in the UBS Machine Learning & Advanced Portfolio Optimization in UBS Quant Insight Series

(Watch replay).

Oct 2020: FinStaR Lab was awarded a grant from HKUST-Kaisa Joint Research Institute on large portfolio optimization.

Sep 2020: Welcome new members Chun Hui and Qingsan Zhu to the lab.

Aug 2020: Welcome new member Jiajun Ma to the lab.

Aug 2020: Dr. Yi Ding has been appointed Research Assistant Professor at the Hong Kong Polytechnic University.

Jul 2020: Prof. Yingying Li presented “Estimating Large Efficient Portfolios with Heteroscedastic Returns” in SoFiE Seminar.

Feb 2020: Welcome new member Leheng Chen to the lab.

Dec 2019: Yi Ding received Dean's PhD Fellowship for Research Excellence 2019-2020.

Nov 2019: Prof. Yingying Li awarded 2019 Excellent Young Scholar, National Natural Science Foundation of China (News in BUSINESS INSIGHT@HKUST and XINHUANET).

Aug 2019: Dr. Bo Zhou has been appointed assistant professor at Durham University.

Jul 2019: Prof. Xinghua Zheng delivered a keynote speech at the 2nd Annual Conference of the Institute of Financial Econometrics and Risk Management of Chinese Society of Management Science and Engineering.

Jul 2019: Prof. Yingying Li was promoted to Full Professor.

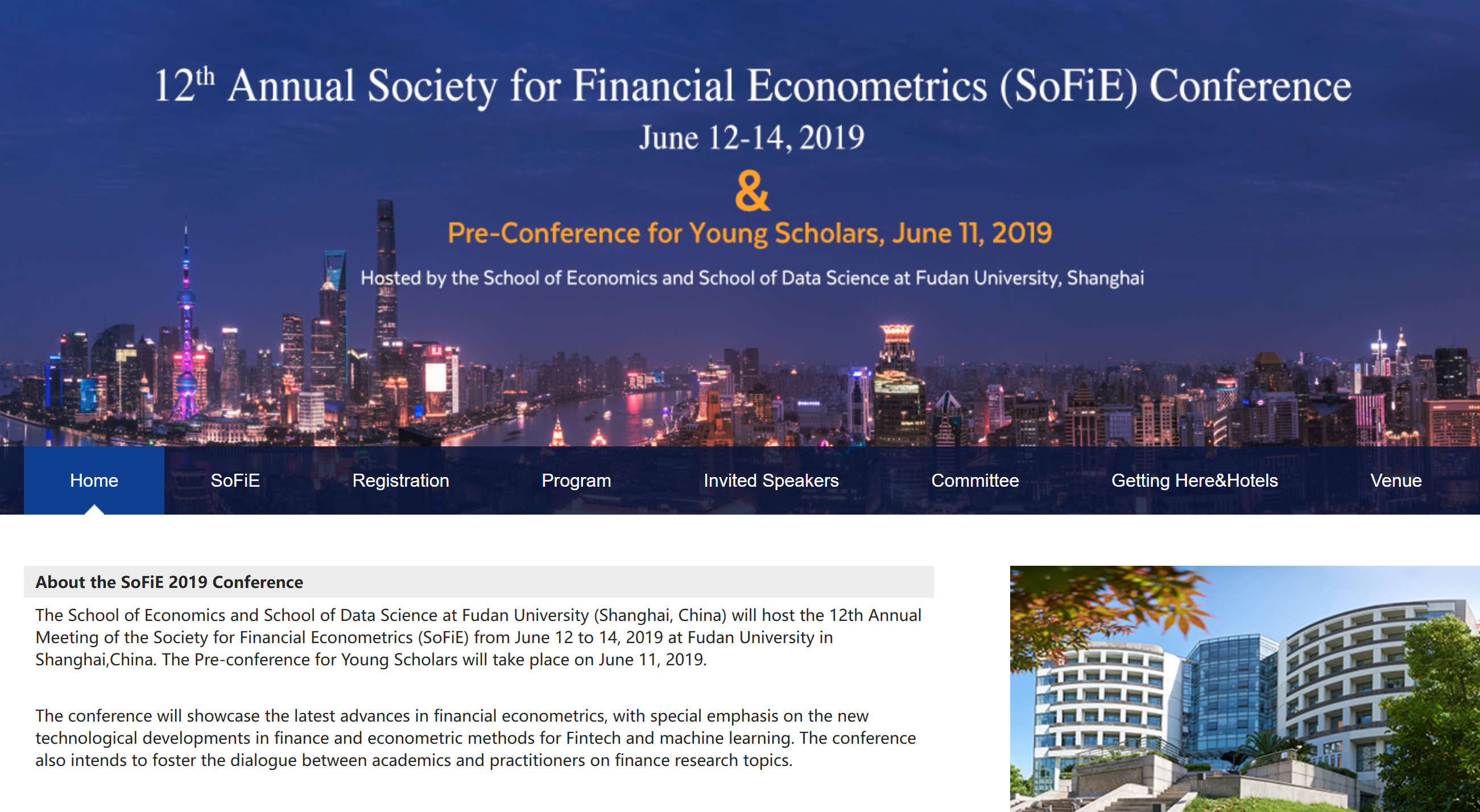

Jun 2019: Prof. Yingying Li delivered an invited theme talk at the 12th Annual Meeting of the Society for Financial Econometrics (SoFiE 2019) in Shanghai. - picture.

Jun 2019: Prof. Yingying Li elected as a Council member of SoFiE.

Jun 2019: Yi Ding received SoFiE 2019 Shanghai Conference Travel Grant from New York University.

May 2019: Wen Luo has been employed as a FOF analyst at ZIAsset.

Dec 2018: Prof. Yingying Li was recognized as one of the faculty members who made exceptional achievements in the past academic year. - picture.

Oct 2018: Welcome new members Changlei Lyu and Lingling Zhao to the lab.

Sep 2018: Prof. Yingying Li has been appointed AE of Journal of Business & Economic Statistics.

Aug 2018: Dr. Xinxin Yang has been appointed assistant professor in C.U.F.E.(中央财经大学).

Aug 2018: Welcome new members Juncheng Li and Guoli Liu to the lab.

Jul 2018: Welcome new member Wen Luo to the lab.

Aug 2017: Welcome new member Bo Zhou to the lab.

Aug 2017: Dr. Xinxin Yang successfully defended her PhD thesis.

Aug 2017: Yi Ding successfully defended Master thesis.

Aug 2017: Prof. Yingying Li served as a judge for the final round of HSBC Financial Dialogue FinTech Challenge.

Jul 2017: Yi Ding received Research Travel Grant of HKUST 2016-17.

Jun 2017: Prof. Yingying Li elected SoFiE Fellow.

Jun 2017: Prof. Xinghua Zheng has been appointed AE of Statistica Sinica.

Jan 2017: Prof. Yingying Li has been appointed AE of Journal of Econometrics.

Jan 2017: Prof. Yingying Li has been appointed AE of Journal of Financial Econometrics.